Coliving

Why Gen Z Is Choosing Coliving in 2026: The Complete Decision Guide

By Mayank Pokharna (Coliving Expert)

• 6 min read

Mar 12, 2026

Share

Key Takeaways

- Solo living isn’t aspirational for Gen Z

- Coliving is structured, not random.

- Gen Z asks five critical questions before committing.

- Friction kills conversions at the decision stage.

- FinTech is a key enabler.

- Retention and referrals are the real growth engine.

Solo Living Wasn’t the Dream. It Was Just the default

For most of Gen Z, the script of adulthood went like this: finish school, get a job, find your own place. Solo apartment. Independence. Freedom. But somewhere between the first rent payment and the second month of eating cereal alone on a Tuesday night, a different question started surfacing: what if there’s another way?

Coliving isn’t new. Communes, boarding houses, and student dorms have existed for generations. What is new is the scale and intentionality with which Gen Z is coming to it in 2026: not as a budget compromise, but as a deliberate rejection of isolation-as-status. With average rents in London, New York, and Bangalore hitting record highs, and AI-powered housemate matching removing the old anxiety of living with strangers, the barriers to coliving are falling just as the appeal is accelerating.

The Loneliness Economy Is Real

Post-pandemic, something shifted. The walls of a solo apartment that once felt like freedom began to feel like a sentence. Zoom calls replaced offices. Delivery apps replaced roommate dinners. And the cumulative financial and emotional cost of going it alone started showing up in bank accounts and therapy sessions alike.

Gen Z drew a different conclusion than the generations before them: privacy is not the same as peace, and independence is not the same as thriving. Co-living is their answer to a housing market that prices out community and a social landscape that defaults to isolation.

What Is Coliving, Actually?

Coliving is purpose-built shared housing in which residents have private bedrooms and share common spaces, kitchens, lounges, coworking areas, and rooftops. Unlike traditional flat-sharing, coliving spaces are managed end-to-end: furnished, utilities included, maintenance handled, and community events organised.

The key distinction from traditional house shares: you don’t find random strangers on Craigslist. You join a curated community, and this is the part that resonates deeply with a generation that values ‘vibe fit’ as much as square footage.

They’re Intrigued. Now They’re Asking the Hard Questions.

Once Gen Z starts seriously exploring co-living, the questions get sharper. They’ve moved past ‘what is this?’ and into ‘is this actually right for me?’ This is the comparison phase, and it’s where most co-living brands lose potential residents by failing to address real anxieties head-on.

The consideration stage is defined by research, comparison, and internal negotiation. They’re weighing co-living against getting their own place, against other co-living brands, and against their own fears about privacy, compatibility, and cost. In 2026, with more Gen Z-native co-living operators than ever before, the comparison landscape is more competitive, and the need to address these fears directly and transparently is the single most effective conversion lever at this stage.

The Five Questions Gen Z Always Asks Before Choosing Coliving

Question 1: Who will I actually live with?

Gen Z doesn’t want to wing it. They want to know how housemates are matched by age, by lifestyle, by work schedule. The word ‘curated’ matters enormously here. Platforms that show their matching methodology questionnaires, lifestyle tags, and quiet hours preferences convert significantly better than those that use ‘we’ll find you great people’ vagueness.

Question 2: How much control do I have over my space?

Private rooms are non-negotiable. The ability to lock a door, not be surprised by a stranger in the kitchen at 6 am, and have quiet when needed, these are baseline requirements, not luxury asks. Coliving brands that emphasise private room quality, soundproofing, and genuine privacy controls convert better with this cohort.

Question 3: What’s actually included in the price?

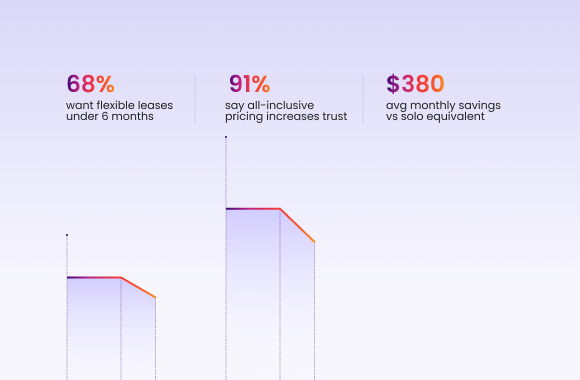

Pricing opacity kills conversion. Gen Z grew up watching subscription traps and hidden fees erode trust in brands. All-inclusive pricing rent, utilities, WiFi, cleaning, and maintenance is not just a feature, it’s a trust signal. Displaying a clear all-in monthly number prominently converts faster than a starting-from price with asterisks.

Question 4: How flexible is the commitment?

Traditional 12-month leases feel like a trap to a generation that changes jobs, cities, and life situations frequently. Month-to-month options, 3-month minimums, or flexible exit windows with reasonable notice periods are strong conversion levers. The flexibility signal reduces perceived risk and accelerates decision-making.

Question 5: Is it actually worth the cost?

The value calculation matters enormously. When you add up solo rent plus utilities plus furniture plus WiFi plus the documented financial and mental health cost of isolation, co-living often wins outright, but you have to do that maths explicitly and visibly for the prospective resident. A cost calculator embedded on the consideration page is one of the highest-converting tools in the coliving marketing stack.

The Role of FinTech in Reducing Consideration-Stage Friction

Here’s where the story gets interesting for financial products. The barriers to co-living aren’t just emotional, they’re financial. Large security deposits, credit checks with strict thresholds, and opaque fee structures are conversion killers at the consideration stage. FinTech embedded into co-living onboarding can remove all three friction points simultaneously.

Deposit-replacement products, alternative credit scoring using open banking data, and instant digital identity verification don’t just help operators reduce defaults they directly address the biggest financial anxieties Gen Z has about committing to a new space. When consideration-stage content explains these options clearly, the decision stage becomes faster and more confident.

They’re Ready. Don’t Let Friction Kill the Conversion.

At the decision stage, Gen Z has done its research. They know what co-living is, they’ve compared options, and they’ve addressed their fears. Now they’re ready to act, and this is where many operators fumble. A clunky application process, an unexpected deposit requirement, or a non-responsive touchpoint can lose a conversion that took weeks to build.

Decision-stage content and UX need to be ruthlessly frictionless. Every step of the move-in journey should feel as easy as ordering something on Depop. For co-living operators, this stage is a product design problem as much as a marketing one, and for FinTech companies, it is the highest-leverage intervention point in the entire resident journey. In 2026, Gen Z applicants who encounter friction here will simply move to the next operator: the choice set is wide, and their tolerance for clunky onboarding is effectively zero.

What Seals the Deal for Gen Z Coliving Conversions

Digital-first onboarding

The entire application ID verification, lease signing, and deposit payment should happen on a phone in under 15 minutes. Document upload, e-signature, and instant confirmation are table stakes. Operators still using PDF forms and email chains are losing Gen Z applicants to competitors with modern onboarding within the same day.

Deposit flexibility

A $2,000–$3,000 security deposit is a deal-breaker for many Gen Z renters who are cash-constrained at the point of move-in. Deposit-replacement products — where a small monthly fee replaces a lump-sum deposit — or BNPL options for deposits can be the final nudge that converts a hesitant prospect into a signed resident. This is the highest-leverage FinTech opportunity in the co-living stack.

Move-in speed

Gen Z moves fast and expects systems to move with them. Flexible move-in dates, available units shown in real time, and instant confirmation emails all signal that you operate like a modern company. Operators who say ‘we’ll get back to you in 3–5 days’ after an application are setting up a cancellation, not a conversion.

Community preview before signing

Before signing, let them see the community they’re joining. A brief intro to current residents, an invitation to a shared group chat, or a link to an upcoming community event, these micro-moments of connection before move-in dramatically reduce last-minute cancellations and early-notice departures.

The FinTech Stack That Closes Coliving Deals

For FinTech companies building in this space, the decision stage is the highest-leverage moment in the entire resident journey. Products that directly address the three biggest conversion barriers, deposit friction, credit access, and verification complexity, can become deeply embedded infrastructure for coliving operators. The most effective FinTech interventions at this stage: instant KYC via selfie plus ID scan (sub-2-minute verification); alternative credit scoring using rent payment history and open banking transaction data rather than traditional credit bureau scores; and deposit-as-a-service products that replace a $2,000–$3,000 lump sum with a small recurring monthly premium. These aren’t add-ons to the co-living stack; they are the infrastructure that makes modern co-living scalable at the pace and volume Gen Z represents.

Decision-Stage Content That Works

- Step-by-step ‘how to move in’ guides with realistic timelines – target ‘how to apply for a coliving apartment online.’

- Transparent pricing pages with zero hidden surprises -deposit amount, cleaning fees, and admin fees all visible upfront

- Testimonials from residents who were initially hesitant – social proof targeting the consideration-to-decision gap

- Live availability calendars and instant booking confirmation -removes uncertainty about unit availability

Deposit calculator showing BNPL vs lump sum comparison with monthly cost difference, targets ‘co-living no security deposit options.

They Moved In. Now Make Them Stay and Refer.

The co-living lifecycle doesn’t end at move-in. For Gen Z, a generation that chooses products and services almost entirely through peer recommendations and social proof, a happy resident is worth five marketing campaigns. In 2026, as AI-generated property recommendations become the primary discovery channel for new renters, authentic resident voices and community reputation carry more algorithmic weight than ever. Retention and community investment aren’t just good culture. It’s the growth engine.

The referral loop is the most powerful customer acquisition channel available to coliving operators, and it costs a fraction of paid acquisition. Every touchpoint after move-in is an investment in future inventory fill rates. Operators who treat retention as an afterthought are leaving their most efficient growth channel untouched.

Retention Plays That Drive LTV for Co-Living Operators

- Resident referral programmes with meaningful incentives – rent credits, free months, or priority room upgrades for successful referrals. Targets ‘coliving referral programme rent credits.

- UGC campaigns: encourage residents to share authentic life-inside-the-community content. Gen Z trust UGC from peers 4× more than brand-produced content.

- Lease renewal rewards: loyalty pricing, room upgrade priority, and location transfer rights for long-term residents. Targets ‘how to renew co-living lease Gen Z’.

- Community ambassador programmes that turn engaged residents into paid local brand voices -sourcing both leads and authentic content simultaneously.

- Transparent early renewal process: notify 90 days out, offer loyalty rate, make saying yes a 2-tap mobile experience.

FAQ

Gen Z is choosing coliving because it solves two problems simultaneously: the financial burden of solo renting (utilities, WiFi, furniture) and the post-pandemic loneliness epidemic affecting 73% of their generation. Co-living offers all-inclusive pricing that averages $380/month less than equivalent solo apartments, plus built-in community, flexible leases, and digital-first onboarding that matches Gen Z’s lifestyle.

Coliving is purpose-built shared housing where residents have private, lockable bedrooms and share common spaces — kitchens, lounges, coworking areas. Unlike traditional house-sharing, coliving is managed end-to-end: fully furnished, all bills included, maintenance handled, and community events organised by the operator. Residents are matched by lifestyle and interests rather than found through classified ads.

Yes, in most major cities. When you combine solo rent, utilities, WiFi, furniture costs, and the financial impact of isolation, coliving averages $380 per month less than an equivalent solo apartment. 40% of Gen Z renters spend over 30% of their income on solo housing — co-living’s all-inclusive model significantly reduces that burden while adding community and amenities.

Gen Z coliving priorities, in order: (1) private room with lockable door — non-negotiable; (2) all-inclusive transparent pricing with no hidden fees; (3) flexible lease under 6 months; (4) fully digital application and onboarding — under 15 minutes on mobile; (5) curated housemate matching by lifestyle and interests; (6) fast move-in availability; (7) community events and common spaces that don’t require forced socialisation.

68% of Gen Z renters want flexible leases under 6 months. Most modern coliving operators now offer 1-month, 3-month, or 6-month minimum terms with rolling month-to-month options thereafter. Some operators offer week-to-week options for digital nomads and short-term movers. Flexible lease terms are consistently ranked as the second most important decision factor after private room quality.

Yes. In 2026, the majority of modern co-living operators use alternative credit assessment methods rather than traditional bureau checks. These include rent payment history, open banking transaction data, and AI-powered income verification via instant digital ID scan making co-living significantly more accessible to recent graduates, international movers, and younger renters with limited credit history than any other form of private rental.