Financial services are no longer experimenting with Generative AI. By 2026, it has become a core capability shaping how banks, fintech startups, insurers, and payment platforms design products, manage risk, and interact with customers. What makes Generative AI in fintech different from earlier automation waves is not speed or scale alone. It is the ability to reason, generate, contextualize, and adapt across complex financial workflows that were traditionally human dependent.

This guide explains how AI in fintech actually works, where it delivers real value, how modern architectures are built, and what impact it is having on the industry in 2026, beyond the surface level hype.

What Generative AI Means in the FinTech Context

A 36-page report highlighting the state of generative AI models including technology overview. Generative AI refers to models that can create new outputs such as text, code, simulations, recommendations, or decisions based on learned patterns. In fintech, this capability goes far beyond chatbots.

Unlike traditional rule based or predictive AI, generative AI systems can:

- Interpret unstructured financial data

- Generate context aware responses and actions

- Adapt outputs based on regulatory, behavioral, and risk constraints

- Learn from feedback loops in near real time

This makes AI in fintech suitable for high stakes domains such as compliance, fraud detection, credit decisioning, financial advisory, and operational intelligence.

Why Generative AI Is Reshaping FinTech in 2026

Three forces have converged to make generative AI central to fintech today.

First, financial institutions now sit on massive volumes of structured and unstructured data including transactions, contracts, customer interactions, and regulatory documents. Generative models are uniquely capable of extracting meaning across these datasets.

Second, customer expectations have shifted. Users expect real time, personalized, conversational financial experiences that traditional systems cannot deliver efficiently.

Third, the regulatory complexity has increased. Institutions need systems that can interpret, explain, and adapt to evolving rules rather than hard coded compliance logic.

Generative AI addresses all three by acting as a cognitive layer across financial systems.

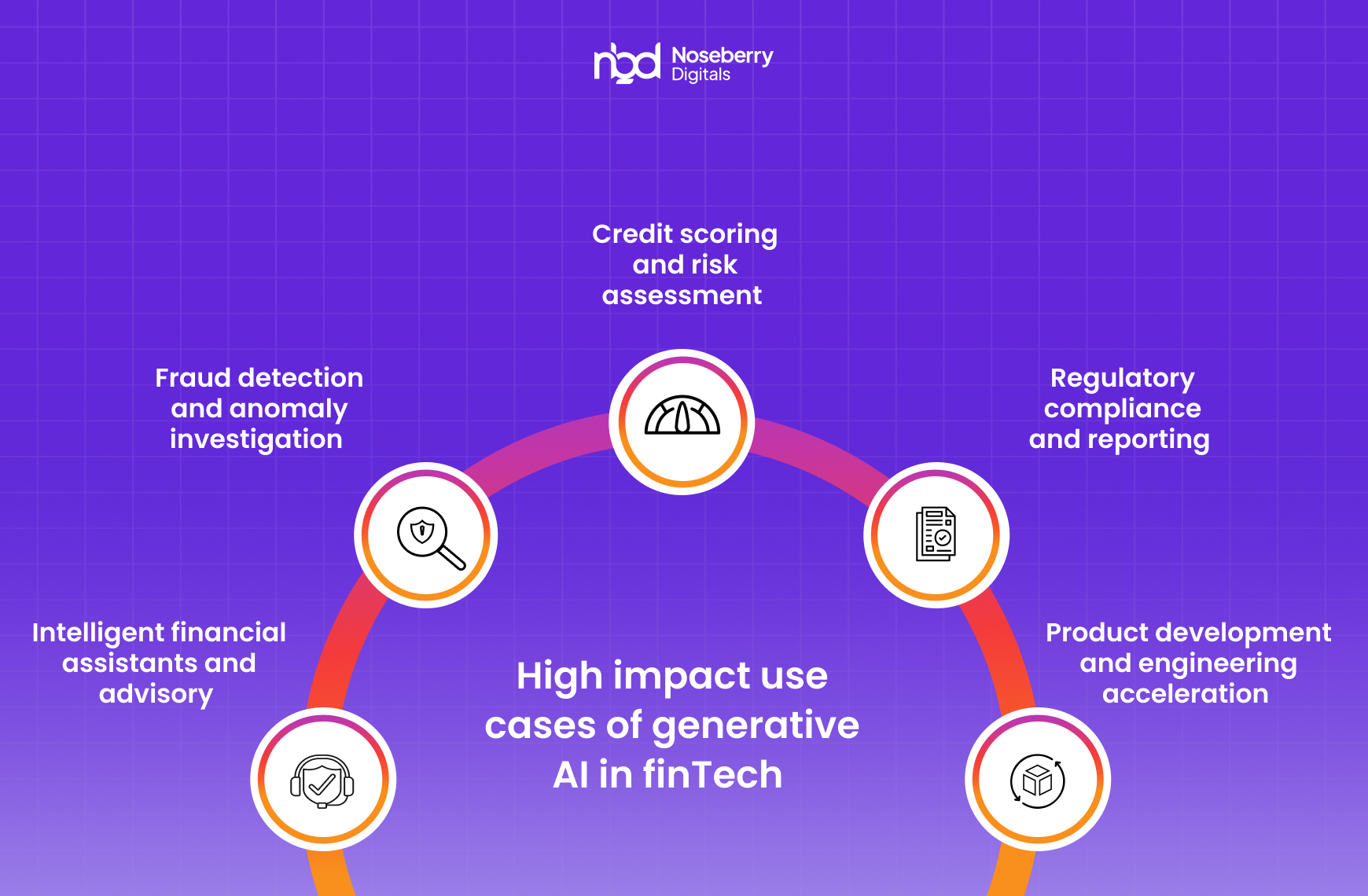

High Impact Use Cases of Generative AI in FinTech

Intelligent Financial Assistants and Advisory

Generative AI enables financial assistants that understand user context, financial history, goals, and constraints. Unlike scripted bots, these systems can:

- Explain complex financial concepts in simple language

- Generate personalized investment or budgeting guidance

- Adapt advice based on changing market conditions or user behavior

The key shift is from reactive support to proactive financial guidance.

Fraud Detection and Anomaly Investigation

Traditional fraud systems rely on predefined rules or anomaly thresholds. Generative AI adds a reasoning layer by:

- Interpreting unusual transaction patterns in context

- Generating explanations for why activity appears risky

- Assisting analysts with investigation summaries and next steps

This reduces false positives while improving investigation speed and accuracy.

Credit Scoring and Risk Assessment

Generative AI in fintech is increasingly used to augment credit decisions by:

- Interpreting alternative data sources such as transaction narratives or behavioral signals

- Simulating risk scenarios under different economic conditions

- Generating transparent explanations for approval or rejection decisions

This improves inclusion while maintaining regulatory defensibility.

Regulatory Compliance and Reporting

Compliance is one of the most impactful areas for generative AI adoption. Models can:

- Interpret regulatory texts and map them to internal controls

- Generate compliance reports and audit summaries

- Assist teams in identifying gaps or potential violations proactively

The value lies not just in automation, but in interpretability and traceability.

Product Development and Engineering Acceleration

Fintech teams use generative AI to:

- Generate and review code for financial applications

- Create test cases for complex transaction flows

- Simulate user behavior and edge cases before launch

This shortens product cycles while improving reliability.

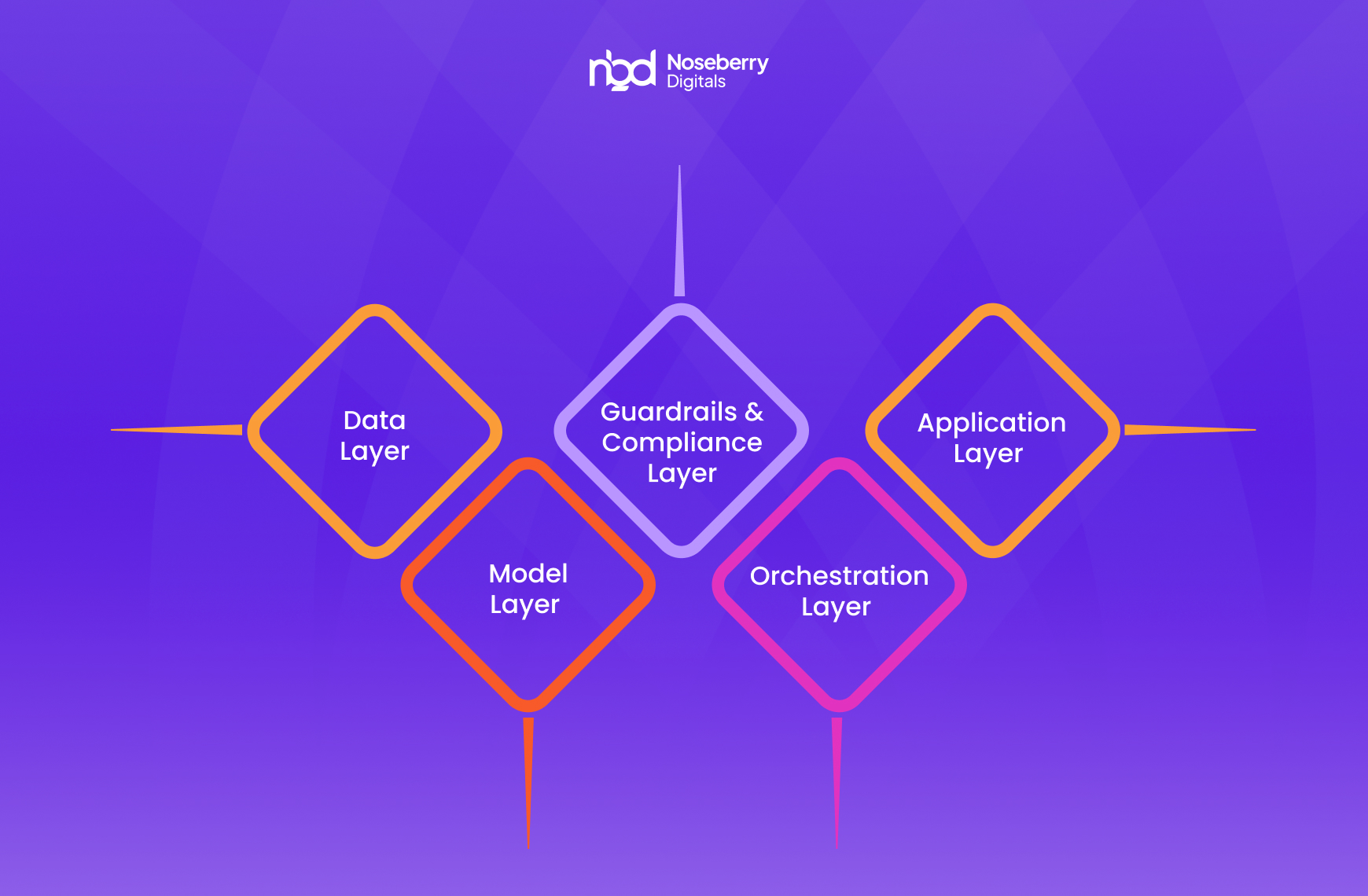

A Practical Architecture for Generative AI in FinTech ‘

A common mistake is treating generative AI as a standalone tool. In mature fintech environments, it is embedded within a layered architecture.

Data Layer

This includes transaction data, customer profiles, logs, documents, and third-party data sources. Strong data governance and lineage tracking are essential.

Model Layer

Typically combines:

- Foundation models for language and reasoning

- Domain fine-tuned models for financial context

- Risk constrained models for sensitive decisions

Orchestration Layer

This layer manages prompts, workflows, validation rules, and escalation paths. It ensures AI outputs are aligned with business and regulatory requirements.

Guardrails and Compliance Layer

Includes:

- Bias detection

- Explainability frameworks

- Human in the loop controls

- Audit logging

Application Layer

Where AI capabilities surface as features such as advisors, dashboards, alerts, or automation tools.

This architecture ensures generative AI enhances systems rather than operating as an uncontrolled black box.

Original Insights Most FinTech Articles Miss

Generative AI Is a Decision Partner, not a Decision Maker

In regulated finance, fully autonomous AI decisions are rare. The real value comes from AI that supports human judgment by generating context, scenarios, and explanations.

Prompt Design Is Now a Financial Control

In 2026, prompts are treated as controlled artifacts similar to business rules. Poor prompt design can introduce compliance or risk issues just as easily as faulty code.

Information Gain Matters More Than Model Size

Larger models do not automatically create better fintech outcomes. Systems that integrate proprietary data, feedback loops, and domain constraints outperform generic implementations.

Explainability Is a Competitive Advantage

Institutions that can clearly explain AI-driven decisions to regulators and customers build trust faster and scale adoption more safely.

Risks and Limitations to Consider

Generative AI in fintech also introduces real risks:

- Hallucinated outputs in sensitive contexts

- Bias amplification if training data is unbalanced

- Over reliance on AI generated recommendations

- Regulatory uncertainty in certain jurisdictions

Successful organizations address these through governance, monitoring, and human oversight rather than attempting full automation.

The Real Impact of Generative AI in FinTech Going Forward

By 2026, generative AI in fintech is no longer about novelty. It is about cognitive leverages. Institutions that treat it as a strategic capability, supported by strong data foundations and governance, gain faster decision cycles, better customer experiences, and more resilient compliance operations.

The winners will not be those who deploy the biggest models, but those who integrate intelligence responsibly into the core of their financial systems.